SMM May 29 Report:

Metal Market:

As of the midday close, domestic base metals all fell, with SHFE copper, SHFE aluminum, and SHFE zinc posting slight declines, all within 0.1%. SHFE lead fell by 0.18%, SHFE tin by 1.59%, and SHFE nickel by 0.74%.

In addition, alumina fell by 2.06%, lithium carbonate by 2.82%, silicon metal by 1.43%, and polysilicon by 2.73%.

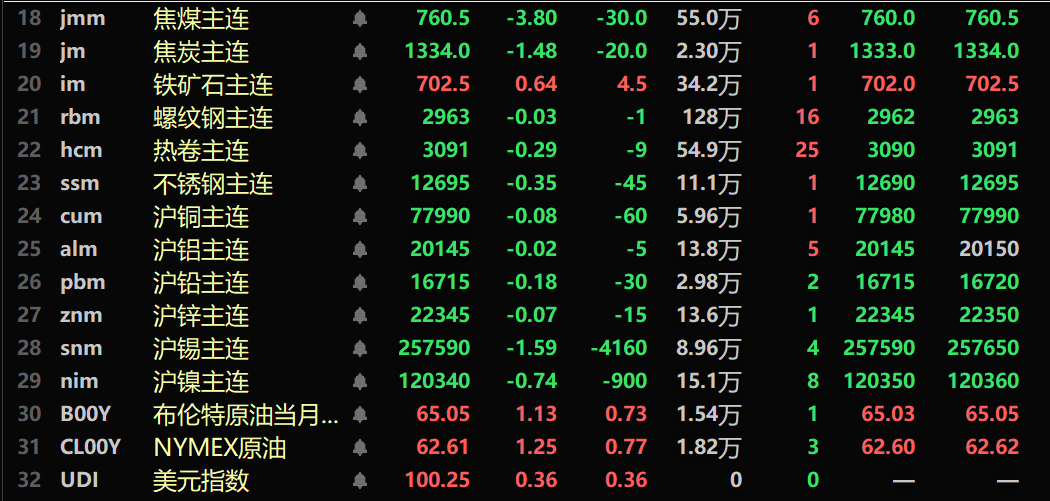

Most ferrous metals series also fell, with iron ore rising by 0.64%, rebar posting a slight decline, and HRC falling by 0.29%. Stainless steel fell by 0.35%. For coking coal and coke: coking coal continued its downward trend from the previous nine trading days, falling by 3.8%, while coke fell by 1.48%.

In overseas metal markets, as of 11:41, LME metals generally rose, with LME copper up by 0.23%, LME aluminum down by 0.1%, LME lead posting a slight decline, LME zinc up by 0.52%, LME tin up by 0.27%, and LME nickel up by 0.93%.

In precious metals, as of 11:41, COMEX gold fell by 0.73%, while COMEX silver rose by 0.44%. Domestically, SHFE gold fell by 0.78%, and SHFE silver posted a slight increase.

As of the midday close, the most-traded contract for the European container shipping index rose by 0.41%, closing at 2012.1 points.

As of 11:41 on May 29, midday futures market movements for some contracts:

》SMM Metal Spot Prices on May 29

Spot and Fundamentals

Copper: Today in Guangdong, spot #1 copper cathode was quoted at a premium of 30 yuan/mt to 100 yuan/mt against the front-month contract, with an average premium of 65 yuan/mt, down 55 yuan/mt from the previous trading day. SX-EW copper was quoted at a discount of 30 yuan/mt to 10 yuan/mt, with an average discount of 20 yuan/mt, down 50 yuan/mt from the previous trading day. The average price of #1 copper cathode in Guangdong was 78,365 yuan/mt, down 150 yuan/mt from the previous trading day, while the average price of SX-EW copper was 78,280 yuan/mt, down 145 yuan/mt from the previous trading day. Spot Market: Today, inventory in Guangdong ended a two-day decline and increased significantly, mainly due to increased arrivals and reduced outflows from warehouses. Downstream replenishment demand was not high ahead of the Dragon Boat Festival, so suppliers had to continuously lower prices to facilitate sales, causing premiums to continue to decline... 》Click for details

Macro Front

Domestic:

[Announcement: The China Council for the Promotion of International Trade (CCPIT) will hold its regular May press conference from 10:00-11:00 AM on May 30]The CCPIT will organize its regular May press conference at the CCPIT Auditorium from 10:00-11:00 AM on May 30 (Friday). Zhao Ping, the CCPIT spokesperson, will release the following: the Global Economic and Trade Friction Index for March 2025, commercial certification data for the national trade promotion system in April 2025, the "Business Environment Report on Japan 2024" and the "Business Environment Report on South Korea 2024", outcomes of the 2025 Global Trade and Investment Promotion Summit, and a preview of events for the Osaka Expo, among others.

[MIIT Releases 2025 Work Plan for Formulating Regulations]The Ministry of Industry and Information Technology (MIIT) has released its 2025 work plan for formulating regulations. Among the projects to be submitted to the ministerial meeting for deliberation this year are the Interim Measures for the Comprehensive Utilisation Management of Scrap Power Batteries from New Energy Vehicles and the Interim Measures for the Total Volume Control and Management of Rare Earth Mining and Smelting and Separation. Projects to be urgently researched and drafted include the Administrative Measures for the Recycling and Comprehensive Utilisation of Lithium-ion Batteries from E-bikes and the Implementation Rules for the Approval of Domestic Entities Leasing Overseas Satellite Resources.

The People's Bank of China conducted 266 billion yuan of 7-day reverse repo operations today, with an operating interest rate of 1.40%, unchanged from the previous rate. As 154.5 billion yuan of 7-day reverse repos matured today, a net injection of 111.5 billion yuan was achieved.

US Dollar:

As of 11:41, the US dollar index rose by 0.36% to 100.25. After the US Federal Court blocked the implementation of the tariff policy announced by US President Trump on "Liberation Day" (April 2), the US dollar rebounded, and market risk appetite improved. According to CCTV News, the US Federal Court blocked the implementation of the tariff policy announced by US President Trump on "Liberation Day" (April 2) and ruled that Trump had overstepped his authority by imposing across-the-board tariffs on countries that export more to the US than they import. It is understood that the Trump administration filed a notice of appeal within minutes of the ruling. White House spokesperson Kush Desai strongly condemned the ruling, stating that unelected judges have no authority to decide how to properly respond to a national emergency, and that the Trump administration will use all executive powers to address the crisis. The market is focusing on the release of US GDP data later in the day, as well as Friday's personal consumption expenditures (PCE) data and comments from Federal Reserve officials, in search of more clues about interest rates. The Federal Reserve maintained interest rates unchanged at its May meeting. Federal funds rate futures traders believe that the Federal Reserve is most likely to resume interest rate cuts in September.

Data:

Today, data such as the number of initial jobless claims in the US for the week ending May 24, the revised annualised quarter-on-quarter rate of real GDP for the US in Q1, the revised quarter-on-quarter rate of the GDP price index for the US in Q1, the revised annualised quarter-on-quarter rate of the core PCE price index for the US in Q1, the revised annualised quarter-on-quarter rate of consumer spending for the US in Q1, the revised quarter-on-quarter rate of the implicit GDP deflator for the US in Q1 (seasonally adjusted), and the month-on-month rate of the US seasonally adjusted pending home sales index for April will be released. In addition, Bank of England Governor Bailey will deliver a speech at the annual dinner of the Irish Association of Investment Managers.

Crude Oil:

As of 11:41, crude oil futures have all risen, with US oil up 1.25% and Brent oil up 1.13%. The rebound in market risk appetite, coupled with ongoing market attention to potential new measures by the US to curb Russian crude oil supplies and OPEC's decision to increase production in July, has supported oil prices.

OPEC did not make any adjustments to its production policy at its Wednesday meeting but agreed to establish a mechanism to set a benchmark for its oil production in 2027. OPEC sources said that the eight-nation meeting to be held on Saturday may agree to further accelerate the pace of production increases in July. Chevron Corporation has terminated its oil production and some other activities in Venezuela, thereby increasing supply risks.

Later on Thursday, the market will focus on the EIA Weekly Petroleum Status Report. A survey of industry analysts released on Wednesday showed that US crude oil inventories increased by approximately 100,000 barrels last week, distillate inventories increased by approximately 500,000 barrels, and gasoline inventories decreased by approximately 500,000 barrels. Data released by the American Petroleum Institute (API) on Wednesday showed that US crude oil inventories decreased by 4.24 million barrels, gasoline inventories decreased by 528,000 barrels, and distillate inventories increased by 1.3 million barrels in the week ending May 23. (Webstock Inc.)

Spot Market Overview:

Midday reviews of other metal spot prices will be updated later. Please refresh to view~